Why this 2026 Federal Budget feels different for pre‑retirees.

If you are in your 50s, own a couple of investment properties, run a business through a family trust and have built a healthy super balance, the 2026–27 Federal Budget probably landed with a thud.

Negative gearing is being restricted, the 50% capital gains tax (CGT) discount is going, and family trusts will face a 30% minimum tax in a few years. For many AMGENT clients in suburbs like Ivanhoe and Collingwood, the big question is simple: “Is my retirement strategy now broken?”

This article unpacks the key changes and shows why, for most pre‑retirees and business owners, the right response is measured, multi‑year planning – not panic selling. Super remains the anchor.

Big picture: what changed in the 2026 Federal Budget?

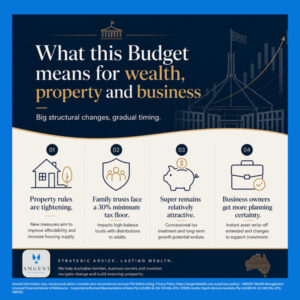

The 2026–27 Budget delivers some of the most significant tax changes for property investors and family trusts in decades. The headline shifts are:

- Negative gearing will be limited to new residential builds from 1 July 2027, with existing properties mostly grandfathered but new established properties losing access to offset losses against wages and other income.

- The long‑standing 50% CGT discount for individuals, trusts and partnerships will be replaced with cost base indexation plus a 30% minimum tax on real gains from 1 July 2027.

- Discretionary (family) trusts will face a 30% minimum tax on taxable income from 1 July 2028, paid by the trustee, with non‑corporate beneficiaries receiving non‑refundable tax credits.

At the same time, the Government is making the $20,000 instant asset write‑off permanent for small businesses from 1 July 2026, and introducing simpler personal deductions and a new Working Australians Tax Offset.

There are no new superannuation tax measures in the Budget itself – but the already‑legislated Division 296 tax on super balances above $3 million starts from 1 July 2026.

1. Property investors: can you still negative gear?

What happens to negative gearing from Budget night?

From Budget night (12 May 2026 at 7:30pm AEST), new property acquisitions are treated differently.

- Existing properties held at Budget night – including properties under contract but not yet settled – keep current negative gearing rules for as long as they are held.

- Established residential properties purchased after Budget night will no longer allow rental losses to offset wages or other non‑property income from 1 July 2027.

- From that date, losses on those established properties can only be used against rental income or property capital gains, with excess losses carried forward to future years.

This means the classic “buy an older unit, heavily gear it, and use the loss to reduce salary tax” strategy is effectively being phased out for new purchases.

New builds are treated differently

Negative gearing remains fully available for qualifying new builds, meaning properties that add to net housing supply – for example, a new dwelling on previously vacant land or a knock‑down rebuild that creates multiple townhouses.

Investors who buy new builds after Budget night will still be able to deduct losses against other income like wages, maintaining the traditional negative gearing treatment. Certain vehicles, including superannuation funds and widely held trusts, are also excluded from the new restrictions.

What this means for a typical AMGENT client

Take a pre‑retiree couple in Ivanhoe in their mid‑50s:

- Two investment properties – one long‑held townhouse and one newer apartment.

- A family trust holding the business, distributing to them and a bucket company.

- Combined income of $280,000, with one property currently negatively geared.

Under the new rules, their existing properties remain fully deductible against salary – they are grandfathered. The bigger question is whether future property purchases (particularly established stock) stack up once the tax benefit is quarantined to property income only.

For most AMGENT clients, this change does not mean “sell everything”, but it does mean being far more selective about any new established purchases and paying closer attention to after‑tax cash flow.

2. Capital gains tax: what happens to the 50% discount?

The old rule

Until now, individuals and trusts who held a CGT asset (such as an investment property or share portfolio) for more than 12 months could generally access a 50% CGT discount on the gain. This has been a cornerstone of wealth strategy since 1999.

The new CGT regime from 1 July 2027

From 1 July 2027, for individuals, trusts and partnerships:

- The 50% discount is abolished.

- Instead, the cost base will be indexed, so only the real (inflation‑adjusted) gain is taxed.

- A 30% minimum tax will apply to capital gains, acting as a floor after indexation.

There are transitional rules for existing assets, so gains may be apportioned between pre‑ and post‑2027 periods under old and new rules. Certain classes, like qualifying affordable housing and some renewable investments, retain or gain special discounts.

Why this matters for pre‑retirees with property

For pre‑retirees who have been counting on selling an investment property or a large shareholding in their 60s to clear debt and top up retirement, the move from a 50% CGT discount to an inflation‑adjusted gain with a 30% minimum tax changes the final number they see at settlement.

It makes the timing of sales, the choice of entity holding each asset, and the balance between super and non‑super wealth much more important than under the old rules.

In practice, it means revisiting questions like: Should one property be sold earlier, while another is kept for longer? Should future growth assets be held in super instead of a family trust? Is there a better mix between direct property, managed funds and business equity? These are not one‑year decisions; they are the basis of a multi‑year exit and retirement plan.

3. Family trusts and bucket companies: the 30% minimum tax floor

What is changing for discretionary trusts?

From 1 July 2028, the Government will introduce a 30% minimum tax on the taxable income of discretionary trusts.

- The trustee will pay tax at 30% on the trust’s taxable income.

- Non‑corporate beneficiaries will still declare trust income in their own returns, but receive non‑refundable credits for the tax already paid at the trust level.

- The policy is framed as preventing wealthy families from paying significantly less tax through income splitting than a worker on a moderate salary, who already faces a 30% marginal rate across a wide income band.

Analysis shows that a large share of trust income currently flows to high‑wealth households, and many family trusts pay effective rates well below 30%, which is exactly what this measure targets.

How this hits “family trust + bucket company” setups

A lot of AMGENT‑style business owners run a structure that looks like this:

- Business trading through a family trust.

- Profits distributed to adult family members on different marginal rates.

- Excess distributed to a bucket company to cap tax at the company rate.

After 1 July 2028:

- Income in the family trust effectively faces a 30% floor, even if distributed to low‑tax‑rate adult children.

- Distributions to a bucket company (already at or around 30%) are less affected, but the interplay with franking, Division 7A and when those profits are eventually drawn personally becomes more important.

- The trust remains valuable for asset protection, control and estate planning, but far less potent as a pure tax‑splitting tool.

The Budget also introduces three years of expanded rollover relief from 1 July 2027, allowing many small businesses and investors to restructure out of discretionary trusts into companies or fixed/unit trusts while still accessing key small business CGT concessions.

What should business owners in Ivanhoe and Collingwood consider?

For SME owners around Ivanhoe, Collingwood and inner‑Melbourne, this is a strong nudge to:

- Review whether the family trust should stay as the main trading and investing vehicle, or whether more profit should be captured at the company level.

- Re‑weigh the value of asset protection and estate planning features of trusts against the new tax reality.

- Use the 2027–2030 restructure window deliberately, rather than waiting until after the minimum tax is already in force.

Again, this is about a structured three‑to‑five‑year plan, not a rushed restructure in 2028.

4. Super stays the centrepiece – even with the $3 million tax

Division 296 in a nutshell

While the 2026–27 Budget did not add new super taxes, the Division 296 “$3 million super tax” has already been legislated and starts from 1 July 2026.

- If a person’s Total Super Balance (TSB) is above $3 million at 30 June, an additional tax applies to the portion of earnings attributed to the balance above $3 million.

- The effective rate on that slice of earnings is about 15% extra, taking it to roughly 30% between $3–10 million and higher above $10 million, but only on the relevant portion – not on the entire fund.

- The $3 million threshold is indexed, so it can increase over time with inflation.

Why super is still central for most pre‑retirees

For the majority of AMGENT clients, even those with healthy balances, super remains the most tax‑effective long‑term retirement vehicle:

- Tax is generally 15% on earnings in accumulation and 0% in pension phase up to the transfer balance cap.

- Super funds, including SMSFs, are not subject to the new 30% minimum CGT tax and are specifically excluded from the negative gearing restrictions affecting individuals and most trusts.

When you line that up against tighter tax settings on personally held property and a 30% minimum tax on family trust income, it reinforces the idea that super should be the core retirement engine, with property, business interests and trusts playing supporting roles in flexibility, legacy and optionality.

5. Small business owners: write‑offs, loss carry‑back and cash‑flow

Permanent $20,000 instant asset write‑off

From 1 July 2026, the $20,000 instant asset write‑off for small businesses with turnover under $10 million becomes permanent.

- Assets costing less than $20,000 (per asset) can be immediately deducted in the year of purchase.

- Assets at or above $20,000 will continue to be depreciated via the simplified small business pool.

- The Government expects this to improve cash flow and reduce compliance costs.

For a Collingwood‑based practice or an Ivanhoe professional firm, this removes the annual “will they or won’t they” Budget announcement and lets owners plan equipment and technology upgrades with more certainty.

Loss carry‑back and other support

The Budget also confirms:

- A permanent two‑year loss carry‑back for companies up to $1 billion turnover from 1 July 2026, letting them apply current‑year losses against taxed profits from prior years within franking constraints.

- A package of small‑business support, including easier tax administration and targeted measures to cut red tape and support investment and innovation.

These are not headline‑grabbing changes, but they do quietly improve the cash‑flow resilience of many AMGENT‑type SME clients.

6. If most of your wealth sits outside super…

Many pre‑retirees AMGENT works with have built wealth the “old‑school” way:

- Business equity in a trust and bucket company structure.

- One or two investment properties (often negatively geared in the early years).

- Super that has grown, but still represents less than half of the total pie.

After this Budget:

- The tax advantages of personal property and discretionary trusts are being squeezed by negative gearing limits, CGT changes and the 30% trust minimum tax.

- Super’s relative attractiveness – even with Division 296 in the background for very high balances – has increased.

For people in their late 40s and 50s, that points towards:

- Re‑balancing over time – gradually shifting more long‑term retirement capital into super (within caps and taking Division 296 into account where relevant).

- Letting personal assets (property, business, trust investments) do more of the work for flexibility, opportunities and legacy, rather than being the sole retirement funding source.

This is exactly the kind of multi‑year pivot that works best when it is mapped carefully and reviewed annually.

7. Case study: Ivanhoe pre‑retiree couple

Consider an Ivanhoe couple, both 55:

- Combined income: $280,000.

- Super: $1.4 million between them.

- Property: home plus two investment properties – a long‑held house and a newer apartment bought in 2024.

- Business: consulting practice run through a family trust with a bucket company.

Under the new settings:

- Their existing investment properties are grandfathered and keep full negative gearing treatment.

- Any new established property purchase after Budget night will have quarantined losses from 1 July 2027, making it much less attractive as a tax‑driven strategy.

- From 1 July 2027, future sales of personally held assets are taxed under the new indexed‑gain plus 30% minimum CGT regime.

- From 1 July 2028, family trust income faces a 30% minimum, limiting the benefit of distributing to low‑income adult children.

A sensible, measured response for them could include:

- Scenario modelling:

- “What if we sell one property before 2027 versus after?”

- “What if one property is moved into super via an SMSF purchase in future?”

- Structure review within the 2027–2030 rollover relief window:

- Should more profit be captured in the bucket company?

- Is the trust still the best main vehicle, or is a company‑led structure better?

- Super strategy:

- Maximising concessional and non‑concessional contributions where appropriate.

- Planning for pension phase and potential Division 296 impacts if balances approach or exceed $3 million.

The outcome is a 3–7 year roadmap, not a series of one‑off reactions.

8. Common client questions about the 2026–27 Budget

“Do I need to sell my investment property now because of the 2026 federal budget?”

Generally, no. Existing properties held at Budget night remain fully negatively geared and are not forced to be sold under these changes. The bigger question is how they fit into a long‑term plan given the future CGT regime and the rest of the portfolio.

“Is my family trust still worth it after the 30% minimum tax?”

For many families, yes – but often for different reasons. Trusts will still be useful for control, asset protection and estate planning, but their role as a tax‑splitting engine will be curtailed by the 30% minimum tax. The decision now hinges more on non‑tax benefits and how the trust fits into the broader structure (including companies and super).

“Should I stop putting money into super because of the DIV 296 tax on $3 million?”

For most people, no. Division 296 affects a relatively small group with very high balances, and even then it only applies to the portion of earnings above $3 million. For the majority of pre‑retirees, super remains the most tax‑effective core retirement vehicle, and the bigger question is how to use remaining working years to build super in a way that fits within the new landscape.

9. How AMGENT helps pre‑retirees and business owners respond – not react

For pre‑retirees and SME owners in Ivanhoe, Collingwood and across Melbourne, this Budget is a structural turning point, not a reason to panic. The goal now is to re‑test the strategy against the new rules and then adjust over time.

AMGENT Wealth Management works specifically with time‑poor professionals, business owners and pre‑retirees in this position, focusing on how super, property, business structures and family wealth all interact. The philosophy is simple: super remains the centrepiece, and everything else is built around it with a measured, multi‑year lens.

To support this, AMGENT provides:

- A growing resources library with explainers on super, structures, retirement and investing:

https://amgentwealth.com.au/resources-wealth-management/ - Practical wealth management tools for pre‑retirees and business owners to stress‑test strategies and scenarios:

https://amgentwealth.com.au/wealth-management-tools/

For many clients, the most valuable next step is a structured Budget impact review that covers:

- Property strategy in light of negative gearing and CGT changes.

- Business and family trust structures in light of the new 30% minimum tax.

- Superannuation and Division 296, making sure super is still doing the heavy lifting for retirement.

From there, AMGENT can help map a calm, staged plan so that as more detail emerges in legislation and ATO guidance, clients are already moving in the right direction rather than scrambling to catch up.

Important information and disclaimer

This article is general information only and does not take into account any person’s objectives, financial situation or needs. It summarises proposed and legislated measures current as at May 2026, which may change before or after becoming law.

Before making any decision about superannuation, property, business structures or investments in light of these changes, readers should seek personalised advice from a qualified financial adviser and, where appropriate, tax and legal professionals.