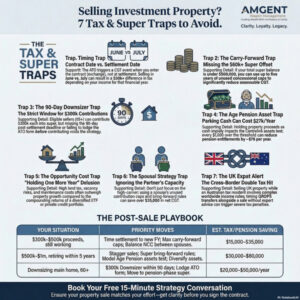

Selling Investment Property Before Retirement? 7 Tax and Super Traps That Can Wipe Out Your Hard-Earned Gains

How Australian pre-retirees, business owners and expats accidentally donate tens of thousands to the ATO and what smart sellers do instead.

Selling investment property before retirement? Let me paint you a picture. It’s a Thursday afternoon. A new client, let’s call him David walks into my office in Collingwood. He’d sold his Northcote investment property six months earlier. $680k settlement. He’d owned it since 2009. Beautiful outcome. Fifteen years of growth, finally realised.

But David wasn’t smiling. His accountant had just called. The CGT bill was $74,000. His super was under-contributed by five years. His wife’s super had barely moved. And the cash sitting in their joint account was quietly eating their Age Pension entitlement, $4,600 a year, gone. Nobody had told them.

“Ben,” he said, “I didn’t know any of this was coming.”

That’s the thing. Most people don’t. Not because they’re careless, David is a smart, successful business owner. But selling an investment property before retirement sits at the intersection of CGT law, super strategy, Centrelink rules and estate planning. It’s genuinely complex. And the mistakes are expensive.

I’m Ben Waite, founder of AMGENT Wealth Management in Melbourne. I’ve spent 20+ years in financial markets, from London trading floors to Australia’s largest super funds to boutique wealth advisory. I’ve guided dozens of clients through exactly this moment. And in this guide, I’m going to walk you through the seven traps I see most often, with real worked examples and what to do instead. Read this before your next accountant meeting.

Why Selling Investment Property Before Retirement Is One of the Most Complex Financial Events You’ll Face

People expect selling investment property before retirement to be straightforward. You sign contracts, settlement occurs, cash arrives. Done. But what happens in the weeks and months around that settlement can determine whether you keep $600k or $500k of it. Whether your Age Pension starts on time or gets delayed. Whether your super grows tax-free or sits under-utilised for another decade.

The rules involved, CGT timing, super contribution caps, downsizer eligibility, the assets test – all interact with each other. A decision made in isolation (sell now, worry about super later) often triggers consequences in a completely different part of your financial life. That’s what makes this moment so important to get right, and why speaking to an adviser before you exchange contracts – not after. This is the smartest call you can make.

With that context, let’s look at the seven traps.

Are you exchanging contracts in June when July saves $25k+?

The trap: Selling Investment Property Before Retirement and the CGT event occurs when you enter the contract (ATO Event A1), not settlement. Exchange in June = FY26 tax return. Exchange July = FY27. Same gain, different marginal rate.

There is nothing worse than have a conversation with a client and telling them their tax planning should have occurred last Financial Year when contracts were signed!

Example: $150k gain, 37% bracket June = $55k tax. 32.5% July = $48k. Saved $7k minimum.

Smart move: Time contract exchange post-July 1 if held 12+ months. Coordinate agent/lawyer/adviser before listing.

- Sell June 2026: $175k income + $180k gain = $355k assessable. CGT component taxed at 47% = $84,600 tax on the gain.

- Sell July 2026: Michael retires in October. Income that year: $60k. $60k + $180k = $240k assessable. CGT taxed at 37% = $54,000 tax.

- Saved: $30,600. One month’s difference in settlement timing.

Smart move: Plan sale timing with both your agent and financial adviser. Know your projected income for both FYs before you set a settlement date. Use the ATO CGT calculator to model both scenarios.

Note: The 50% CGT discount is currently under political discussion in Canberra. As of March 2026 it remains intact but worth monitoring.

Are you missing $60k+ super carry-forward tax offset?

Most people know the super concessional contribution cap – $30,000 per year in FY26, rising to $32,500 from 1 July 2026. What they don’t know is that if they haven’t maxed those caps in previous years, and their total super balance (TSB) is under $500,000, they can carry forward the unused amounts and use them in one hit, up to five financial years of unused caps.

Why does this matter when selling property before retirement? Because concessional contributions are tax-deductible. You claim them as a personal deduction, they reduce your assessable income for the year, and they’re taxed at just 15% inside super instead of your marginal rate of up to 47%. When you’ve just triggered a large CGT gain, carry-forward contributions are one of the most powerful tools available.

Worked example, carry-forward in action:

Sandra, 55, sells a Geelong rental. CGT gain after 50% discount: $120,000. She earns $95k/year as a nurse. Without planning, that $120k is added to her income and taxed at 37% a $44,400 tax bill on the gain alone.

But Sandra’s TSB is $380,000. She hasn’t maxed her concessional contributions for four years. Her carry-forward balance: $68,000. She contributes $68,000 concessionally.

- $120k gain minus $68k deduction = $52k net addition to income

- Tax on $52k at 37% = $19,240

- Tax on $68k inside super at 15% = $10,200

- Total tax: $29,440 vs $44,400 without the strategy. Saved: $14,960.

Smart move: Log into MyGov and check your carry-forward balance before settlement. If your TSB is under $500k, this strategy is almost always worth exploring. Contribute before 30 June of the relevant FY. Work test applies if you’re 67+.

Will your downsizer contribution fail the 90-day rule?

The downsizer contribution is one of the best strategies available to Australians selling property before, in or near retirement. But it’s riddled with rules that trip people up – miss it by a day or a technicality, and you’ve lost it entirely.

If you’re 55 or older and you sell your main residence owned for 10+ years, you can contribute up to $300,000 each ($600,000 per couple) directly into super, completely outside the normal NCC cap of $120,000 per year (rising to $130,000 from 1 July 2026). No total super balance limit. In pension phase, earnings are completely tax-free.

The rules people most often get wrong:

- The 90-day window: Contribute within 90 days of settlement. Not 91. Miss it and the contribution counts as a normal NCC, burning your $120k cap.

- The ATO form: Lodge the Downsizer Contribution Form with your super fund at or before the time of contribution and not afterwards.

- Main residence test: Must be your main residence, not an investment property, no matter how long you’ve owned it.

- 10-year ownership: The property must have been owned for at least 10 continuous years. Calculate carefully with joint ownership.

Worked example, downsizer done right:

Robert and Jenny, both 63, sell the Balwyn North family home for $2.1m. They downsize to a $1.4m apartment. $700k freed up. Modest super balances. Robert $480k, Jenny $310k.

- Robert contributes $300k downsizer → super $780k in pension phase, tax-free earnings

- Jenny contributes $300k downsizer → super $610k in pension phase

- Combined $600k in super at ~7% = $42k/year tax-free

- Done wrong — $600k cash → exceeds March 2026 couple homeowner threshold ($481,500) by $118,500 → Age Pension cut by $9,204/year

Smart move: Before settlement, confirm eligibility with your adviser, download the ATO form, and have your fund ready to receive the contribution. Don’t wait until the cash lands in your account.

Is cash killing your Age Pension by $20k/year?

This one catches people who are cautious by nature, who want to “park the money and think about it.” That instinct is understandable. A large settlement is stressful. But Centrelink doesn’t give you breathing room on the assets test.

From 20 March 2026, the Age Pension assets test thresholds are:

- Homeowner single — full pension up to $295,500, cut-off at $674,000

- Homeowner couple — full pension up to $481,500, cut-off at $1,012,500

Every $1,000 over the full pension threshold reduces your pension by $3 per fortnight, roughly $78/year in lost pension per $1,000 over threshold.

Worked example. The cash trap:

Helen, 68, sells her investment property. Proceeds: $520k. Pre-sale assessable assets: $310k. Post-sale: $830k. That’s $348,500 over the couple threshold. Pension reduction: $348,500 ÷ $1,000 x $3 x 26 fortnights = $27,183/year lost.

If Helen had moved $300k into super (pension phase) and restructured the rest, her assessable assets drop significantly and pension entitlement is largely restored.

Smart move: Before settlement, map your post-sale asset position against current thresholds. The difference between “park as cash” and “invest strategically” easily runs to $15,000–$27,000 per year in pension income.

Is “Holding one more year” costing more than CGT?

This trap feels most logical from the outside. “I’ll hold another year, let it grow, then sell.” Or: “The CGT is too high right now, better to hold.” Both can be true. But they’re also often wrong, and the numbers rarely get properly modelled.

Here’s what “one more year” actually costs in Victoria:

- Land tax: $800–$2,500/year on a $600k property depending on portfolio

- Vacancy risk: One month vacant = 8% of annual rent gone

- Maintenance and rates: Typically 1–2% of property value annually

- Opportunity cost: $600k in a 7% ETF portfolio = $42k/year in growth, compounding

Worked example. Hold vs Sell:

Greg, 57, owns a Footscray rental worth $650k. Net yield: 2.8% after costs ($18,200/year). CGT if sold now: $52,000. He holds two more years.

- Two years income: $36,400. Land tax + maintenance: $8,000. Net: $28,400.

- $598k invested at 8% for two years: grows to $698k. Growth: $100,000.

- Property at 3% annual growth: $689k. Growth: $39k. CGT now larger.

- Holding cost Greg ~$72k in opportunity cost over two years, net of income received.

Smart move: Run a hold vs sell analysis. If net yield is under 4–5% and you’re within 10 years of retirement, selling and redeploying almost always wins on a risk-adjusted basis.

Can I use my spouse’s super? blocking $36k tax savings.

In most relationships, one partner earns more. When a large CGT gain appears, the instinct is to contribute to the higher earner’s super, their tax rate is higher, the deduction saves more. Makes sense in theory. Often misses a better opportunity sitting right next to them.

Super contribution caps apply per person. The NCC cap ($120k in FY26, $130k from 1 July) and bring-forward ($360k in FY26, $390k from 1 July) are individual entitlements. If one spouse’s TSB exceeds the $1.9m transfer balance cap, they can’t make NCCs at all, while the other spouse may have substantial unused capacity.

Worked example. Splitting contributions:

Andrew and Lisa sell their Kew investment property. Gain after discount: $200k. Andrew earns $240k. Lisa earns $65k part-time. Andrew’s TSB: $1.8m. limited NCC room. Lisa’s TSB: $420k substantial room.

- Without advice: Contribute $120k to Andrew. CGT on $200k at 47% = $94,000.

- With advice: $120k NCC to Lisa (bring-forward). Lisa claims $40k concessional carry-forward. Spousal strategies applied. Net CGT reduced by $36,800. Lisa’s super accelerated toward tax-free pension phase.

Smart move: Model both spouses’ contribution capacity before settlement. TSB, unused concessional caps, NCC bring-forward, all need checking at 30 June prior year. A couple is a financial unit. Use both sides.

Can I sell my property and transfer my Pension? Double tax hit coming for UK Expats?

This is specific to a segment I work with closely, British expats in Australia, or Australians returning from the UK with property and pension assets there. The consequences of getting it wrong are severe.

If you’re an Australian tax resident and sell a UK rental property, Australia taxes your worldwide income, including that UK gain. The UK may also tax it. The Australia-UK double tax agreement provides foreign tax credits, but the mechanics are complex, timing mismatches between UK and Australian FYs create additional exposure, and QROPS pension transfers made in the same year as a property sale can create simultaneous taxable events on both sides of the globe.

Worked example. Expat property sale done right:

James, 56, UK citizen living in Melbourne 12 years. Sells UK flat for £380k (bought £190k). £190k gain. Australian tax resident.

- Without planning: UK CGT + Australian CGT + QROPS triggered same year = $80k+ total tax impact.

- With planning: QROPS structured in prior year. Property timed to low-income year. UK tax credit properly claimed. Carry-forward super contributions applied. Total tax: $38k. Saved: $42k.

Smart move: If you have UK property or pension assets, do not sell or transfer without specialist cross-border advice –Read more on UK Expat strategies here. AMGENT works with specialist UK-Australia tax advisers to ensure nothing falls through the cracks.

Your Post-Sale Playbook: Three Paths Forward

| Your Situation | Priority Moves (in order) | Est. Tax / Pension Saving |

|---|---|---|

| $300k–$500k proceeds, still working | 1. Time settlement to new FY 2. Max concessional + carry-forward 3. Balance NCC between spouses 4. Invest surplus in ETFs / private credit |

$15,000–$35,000 |

| $500k–$1m, retiring within 5 years | 1. Stagger sales across two FYs 2. Super NCC bring-forward both spouses 3. Downsizer if main residence 4. Model Age Pension assets test 5. Diversify into ETFs, private credit, commercial funds |

$30,000–$80,000 |

| Downsizing main home, 60+ | 1. Downsizer $300k/person within 90 days 2. Lodge ATO form before contribution 3. Check 12-24m assets test exemption 4. Move to pension-phase super 5. Model Age Pension impact |

$20,000–$50,000/year |

What Getting This Right Actually Looks Like

Let me come back to David. After our first conversation, we couldn’t undo the CGT, it was triggered. But we rebuilt from there. We applied carry-forward contributions to his wife’s super, $58,000 that year. We restructured cash proceeds into a managed portfolio sitting below the Age Pension threshold. We pre-positioned for the downsizer contribution on the family home they planned to sell in two years. And we modelled his retirement income streams clearly for the first time, David could see exactly what his financial life looked like at 65.

The $74k CGT bill still hurt. But the future was structured. No more surprises. That’s what this is about. Not perfection. Clarity.

Frequently Asked Questions

Should i selling investment property before retirement?

In most cases, yes – particularly if net yield is under 5% or you’re carrying significant unrealised gains. The key is timing and sequencing. Selling in the right financial year, with the right super strategy in place, can save $20k–$80k compared to selling reactively. Speak to an adviser before you list, not after you sign contracts or settle.

How is CGT calculated when selling investment property in Australia?

Sale price minus cost base (purchase price, stamp duty, legal fees, capital improvements, selling costs). If held 12+ months, apply 50% discount. Remaining gain added to assessable income for that year. Taxed at your marginal rate, up to 47% for high earners. See the ATO Property and CGT guide.

What are the super contribution caps for FY26 and FY27?

FY26 (to 30 June 2026): Concessional $30,000, Non-concessional $120,000, Bring-forward $360,000. FY27 (from 1 July 2026): Concessional $32,500, NCC $130,000, Bring-forward $390,000. Downsizer $300,000/person unchanged. Div 296 what you need to know and calculator

Will selling my investment property affect my Age Pension?

Yes, proceeds as cash count immediately under the assets test. From 20 March 2026, homeowner couples hold up to $481,500 before pension reduces. Every $1,000 over costs $3/fortnight. Move proceeds into pension-phase super to reduce assessable assets. See Services Australia assets test.

Is it better to sell before or after I retire?

After, if income will drop significantly post-retirement. Selling into a year when your income is $60k instead of $180k can save $20k–$30k in CGT alone. Model both scenarios with your adviser before deciding.

Don’t Let the ATO Take Your Gain

These traps cost Australians tens of thousands every year and not because they’re reckless, but because property sales feel simple and the complexity hides in the rules around them.

If you’re selling investment property before retirement, or thinking about it. The best time to get advice is now. Before contracts. Before settlement. Before the cash lands and the options narrow. Then read about what options you have here

Free 15-minute strategy conversation. No obligation. No jargon. Just clarity.

👉 Book Your Free 15-Minute Conversation

Or ask us about the Property Sale Tax & Super Checklist — a one-page guide that maps your key decisions in under 60 seconds.

Your sale was the hard work. Let’s make sure the outcome matches the effort.

General Advice Disclaimer: The information in this article is general in nature and does not consider your personal financial situation, objectives, or needs. It is not intended as personal financial advice. Before making any investment or financial decision you should seek advice from a qualified financial adviser. AMGENT Wealth Management Pty Ltd holds an Australian Financial Services Licence (AFSL). Past performance is not a reliable indicator of future performance. Tax figures referenced are based on current ATO rules and thresholds as at March 2026 — confirm current rates with your accountant. Centrelink thresholds current as at 20 March 2026.